Thanks to technology, the transition to custom indexing is happening faster than anyone expects

Thanks to technology, the transition to custom indexing is happening faster than anyone expects

A core principle of money and investments is compounding interest. Over the long run, this mathematical truth generates exponential rates of return for investors’ portfolios.

Technology is no different. As with investing, however, there are tradeoffs to compounding—the primary downside with technology being that it replaces a traditionally-human function, displacing the laborer.

At the liminal intersection of compounding technology and investing are “robo-advisors”; a term which I use loosely to define automated portfolio management in general. I understand that’s not the common definition, but it’s getting harder and harder to distinguish between a fully automated process and a mostly-automated process with some human oversight. However you want to define robo-advisor, automated portfolio management is now ubiquitous: from Wealthfront and Betterment (small) to third party tools like Morningstar and Riskalyze (medium) to J.P. Morgan and Goldman Sachs (large).

What is custom indexing (aka direct indexing)?

Direct indexing is a little easier to define than robo-advisor at the moment: it’s an investment portfolio that replicates an index (like the S&P 500), but instead of replicating an index by purchasing a pre-packaged product like an ETF (e.g. SPY), the investor removes that packaging by purchasing a substantial portion of the underlying securities explicitly (e.g. AAPL, MSFT, AMZN, GOOG, TSLA).

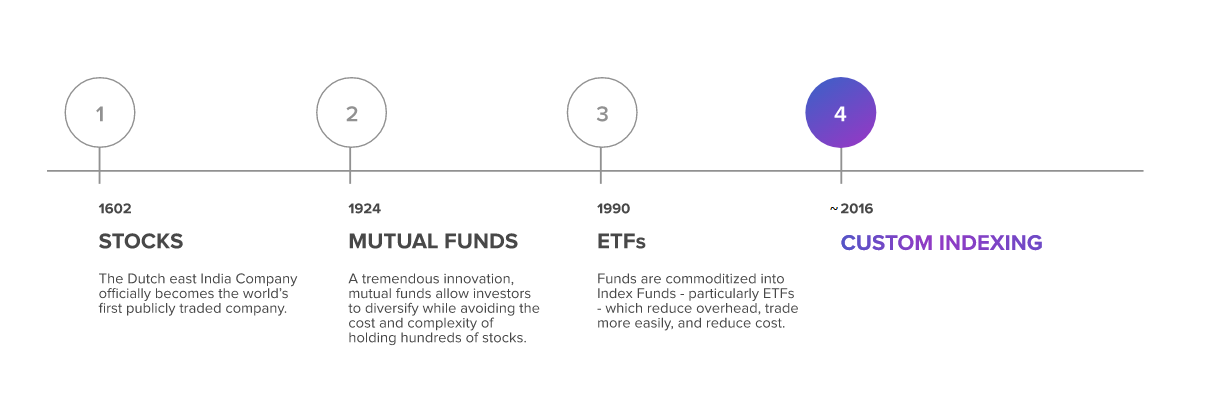

Innovations across hundreds of years in the financial sector have paved the way for custom indexing. Starting in the 17th century, individual stocks were the first form of investing. Without the sophisticated regulation and financial vehicle structure we know today that allows for pooled investments and funds, buying individual stocks was the only option. However, given the high cost to access this type of investing, stocks were inaccessible to the majority of the population.

Then in the 1920s, a more simple and obtainable way for individuals to invest and build a diversified portfolio came along: mutual funds. As mutual funds evolved over time, they were often hailed as a tremendous innovation for offering greater accessibility and diversification than their financial predecessors. The downside for many was that mutual funds often had front-end loads, back-end loads, and much larger tax burdens due to capital gains and trading restrictions.

To reduce that cost and overhead, ETFs made their debut as the innovation of the 1990s. ETFs can be traded like stocks and offer a smaller tax burden in comparison to mutual funds, but they still do not allow for any customization.

This is where custom indexing comes into play. Also known as direct indexing, custom indexing is a tech-centric take on Separately Managed Accounts (SMAs)—tailoring individual account holdings and strategies to end-client preferences efficiently and profitably.

With direct indexing, what’s old is new again and for the first time in a long time, buying individual stocks is back on the table for the majority of the population. This power of customization in an investment portfolio allows for individualized decisions centered around an investor’s values, beliefs, and lifestyle.

The rise of direct indexing

In the early days of direct indexes, the service was primarily reserved for institutional investors and high-net-worth individuals with enough money to pay for manual customization of their portfolio. In order to avoid the tax repercussions of mutual funds, some mutual fund managers would create SMAs that mirrored their own funds for larger clients. This made the service expensive and therefore inaccessible to the masses.

In the last few years, advances in cost structures, technology, and increasing consumer demand have made direct indexing—which was once exclusive to at the high-end of the market—a more attractive and accessible solution.

One of the largest disruptive changes to the investment marketplace was in October 2019 when Charles Schwab eliminated the online trading commission for U.S. stocks, ETFs, and other options. What started with Charles Schwab and other early trendsetters resulted in a market-wide pressure. The broker commissions that were once the prohibitive factor disappeared almost overnight.

Advancements in digital platforms have also improved this accessibility. Automation, for instance, removes the manual labor involved in replicating individual ETF holdings, which enables advisors to create custom-built portfolios for each of their clients efficiently.

Consumer demand has also pushed forward the need for further customization. This survey from Morgan Stanley suggests 86% of millennials are interested in “sustainable investing” and are looking to their advisors for the level of customization they want—centered around personal interests, values, and beliefs.

As direct indexing mainstreams, advisors will begin to differentiate themselves based *not on* an advisor-centric investment edge, but rather on how the model portfolio can best be customized to place the client’s personal situation front and center.

Looking ahead: the problems with indexing and technology

The Center for American Progress recently released a comprehensive overview of problems facing indexing practices; recommending legislative review of certain aspects of the practice. Most of them, if not all of them, revolve around conflicts of interest in esoteric index creation for the benefit of a small group of institutional clients.

Broadly, with passive indexing, the responsibility for portfolio management gets transferred from the heavily-regulated investment manager onto the almost-unregulated index creator.

This method of investing is less passive than one might expect. Some indexes are created and maintained based primarily on objective criteria, and others rely on significant discretion by index administrators. Often, decisions about index construction, including which weights are selected and which particular components are included, are made by committees that retain significant discretion. These decisions about what goes into an index or how it is weighted can have large implications for how money flows to companies or even countries. This discretion, coupled by the meaningful economic rewards enjoyed by companies included in popular indexes, create significant risks for investors, including often significant and documented conflicts of interest, such as the possibility of issuers of securities purchasing services from index providers to attempt to influence index membership.

These conflicts of interest dissipate with custom indexing however, as active portfolio decisions are once again the responsibility of the investment manager (e.g. financial advisor). There are two things stopping direct indexing from taking hold full force:

Cultural adoption by advisors, and

Efficient technological platforms

And if you are a financial advisor reading this blog post, I know you’re not burdened by #1. As for #2, come see what I’m building here:

I’m on a mission to build the interface that enables advisors and clients to effectively collaborate on their investment portfolio strategies and social preferences—all cost competitive with robos and while still profitable for advisors.

Early adopters of my platform have already shaped the direction of the application invaluably, and now you have that same opportunity.

Opportunities and Threats moving forward

From my perspective, there are a few ways “investment management for the masses” plays out.

If you manage ETF models within separately managed portfolios, your main competition are the robos. Frankly, robo-advisors can do that best by far; quantitatively, and at a much lower cost. But if you do join the trend of custom indexing—which is what I’ve been advocating for some time—you have three options:

Accept and utilize multiple, prepackaged solutions by custodians and wirehouses,

Program your own solution in-house for the benefit of a few hundred clients, or

Get in on the ground floor of an independent solution built for RIAs to influence the direction of an application that suits your needs

StockGen is that third option.