📰 Thoughts on the search for alpha

📰 Thoughts on the search for alpha

The search for alpha is a never-ending quest. Years ago, certain factors were “discovered” to deliver incrementally better returns in the long run; small caps and value tilts, for instance. Slowly but surely, as more investors sought fled to this style of investing, these factors stopped outperforming. Such is the difficulty of (semi-)active management. As potential areas of outperformance become widely known, alpha dwindles there and begins to sprout up in other places. Markets evolve into a perpetual cycle of chasing performance factors.

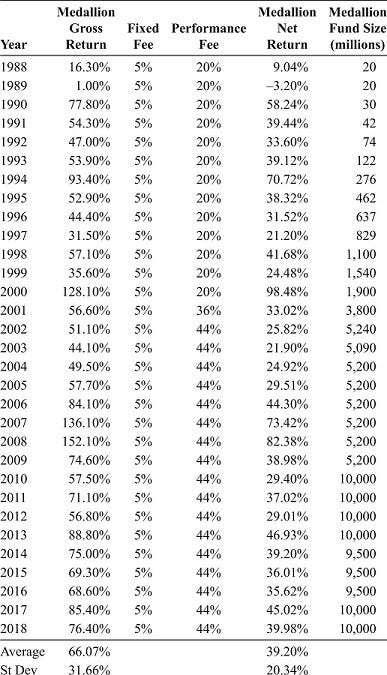

Medallion Fund Performance according to The Man Who Solved the Market (Zuckerman)

According to Jim Simons, Renaissance Technologies is able to achieve such performance only with teams of highly skilled scientists employing machine learning to identify patterns on a time scale of hours-to-days.

I’ve been thinking about the future of investment portfolio performance. While 60/40 had a great year in 2020, I’m not so sure it continues. Interest rates have to be more likely to go up than down in the long run and many valuation metrics suggest equities are overextended here.

The Medallion Fund makes it seem like alpha is unlimited, though. So I wonder if there’s an opportunity between low single digit performance and the 40% annualized Medallion puts up. In fact, I’m pretty sure there’s room for a fluid human-quant strategy in the same way freestyle chess teams can beat their computer-only counterpart.